Last week’s blog got me in a bit of hot water with some alternative investment folks I know. In fact, some thought it should have come with a lifetime supply of chocolate-covered Prozac to counteract the depressive, after-reading effects.

To answer the queries I seemed to receive en masse: No, I am not a defeatist. I am instead an optimistic pessimist – I’m often quite positive that the worst possible thing is bound to happen.

But just because I suggested last week that a few fund managers might have to (or want to) evaluate their long-term business viability in 2016 doesn’t mean I think this year is a total loss.

In fact, I’d say my best advice is, in the infamous words of Douglas Adams, “Don’t panic!” If you can do that and still somehow end 2016 knowing where your towel is, you’ve won.

But seriously, there are a number of positive developments for money managers that could play out this year. For example:

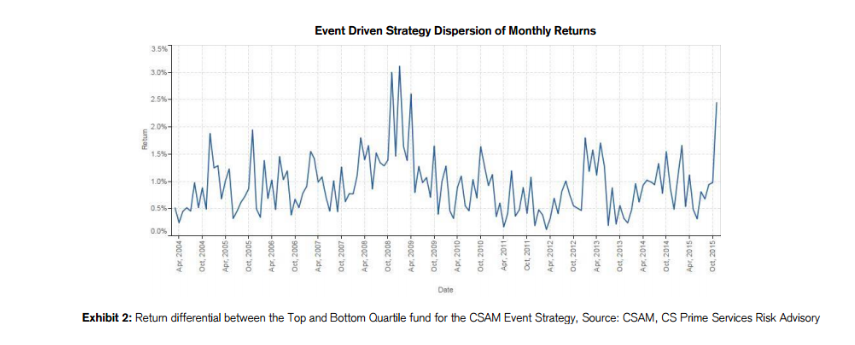

Market Volatility May Be Your Friend – If the stock market theme song post-financial crisis has been “Sweet Child of Mine”, 2016 has certainly changed its tune. Market volatility during the first two weeks of January brought me back to my high school-era living room, sitting in front of my (not flat-paneled) TV watching Axl Rose wiggle across stage belting out “In the jungle. Welcome to the jungle. Watch it bring you to your knnn, knnn, knnn, knnn, knees, knees. I want to watch you bleed!” That was one of my favorite videos back when, you know, MTV actually played music.

And while market volatility can be an exercise in white-knuckle, bile-producing, ‘how-will-I-ever-retire-now’ angst, it also offers investment managers an opportunity they haven’t really had since March 9, 2009: The chance to be a hero.

In a raging bull market, most performance looks like beta. No matter how well an active money manager does, the market can do it faster, cheaper and potentially better. A bull market is often a chump factory, no matter your talents.

And don’t get me wrong, I love a bull market because I am generally in better shape (shopping is, after all, my cardio), but a bull market doesn’t love active management. A down, sideways or otherwise volatile market creates what active money management really needs: Opportunity.

So play this one well, intrepid asset managers, and you could potentially see your breakthrough moment. And may the odds be ever in your favor.

The Fees Knees – Speaking of your knnn, knnn, knnn, knnn, knees, while the markets haven’t exactly been a jungle until recently, the fee debate certainly has. There has been a barrage of class action lawsuits against Fidelity, Vanguard and others about excessive 401(K) fees. And if you Google “hedge fund fees” two of the top three responses are “Hedge Fund Performance Fees Decline Sharply” (FT) and “The Incredibly Shrinking Hedge-Fund Fee” (Bloomberg View).

Due at least in part to the inability of active managers to shine (see above), fees have become a inevitable battle ground for investors. When the rising tide lifts all ships, it becomes easier to confuse price with value.

But market volatility may help successful managers overcome near militant fee resistance, and interestingly enough, a new lawsuit against Anthem Inc. about low fee funds may help traditional active managers as well.

“An overriding theme of lawsuits attacking 401(k) plan fees is that they generally view the cheapest investment as being the most prudent investment choice fiduciaries can make for plan participants, according to Brad Campbell, counsel at Drinker Biddle & Reath and former head of the Employee Benefits Security Administration. That, Mr. Campbell said, is inconsistent with a fiduciary's obligations under the Employee Retirement Income Security Act of 1974, which indicates fees must be reasonable rather than the most inexpensive. According to the text of the new suit's complaint, “investment costs are of paramount importance to prudent investment selection,” which Mr. Campbell said is “an inaccurate statement of the law.” (http://www.investmentnews.com/article/20160112/FREE/160119984/401-k-suit-targeting-vanguard-fees-could-support-case-for-active)

After all, to misquote Brian Tracy, “The true measure of the value of any [money manager] is performance.”

Election Attention – And finally, in case y’all have slept through the proposed UK Trump ban, the Sanders-Clinton (oh, yeah, and O’Malley) poll mania, and impassioned pleas for walls around the country or just around Wall Street, you know we’re in an election year. Why is this a good thing? Well, for one, it’s wildly entertaining, although it does bring to mind PoliSci 401 “Those who seek power are not worthy of that power.” (Plato)

But really, it means the Eye of Sauron (read: regulatory and compliance entities) may be thinking about Wall Street, but it is unlikely that much will change this year, giving everyone a chance to continue working through compliance, operations, Form PF, AIFMD, and all of the other special gifts fund managers have gotten post 2008. Hell, someone may even come up with a way to streamline some of those processes during the short lull in activity and actually create some true economies of scale for struggling small funds. It’s MLK day (er, night) as I’m writing this so well, dammit, I have a dream.

In short, it ain’t all doom and gloom out there for the financial industry, but if this blog failed to convince you of that, I can only offer the following to answer any of your lingering doubts or questions.